Security fears ‘putting people off’ contactless mobile payments

Nearly half of smartphone users do not want to use their device to make contactless payments, mostly over fears about security, according to a survey.

Nearly half of smartphone users do not want to use their device to make contactless payments, mostly over fears about security, according to a survey.

The growth of mobile money has been a steep upward curve and looks set to continue – Juniper Research predicts that there will be one billion mobile banking users worldwide by the end of 2017, up from 590 million in 2013. A recent Forrester report predicted that purchases on mobile devices would double by 2018, as even more people become comfortable buying online and retailers create more user-friendly mobile experiences

On the background of a recent study revealing that UK mobile banking users are set to double to 32.5 million by 2020, banks need to tailor their customer experience models heavily towards mobile devices, with the fundamental focus on creating a “mobile-first” strategy, if not the more radical “mobile-only” strategy

As mobile handsets become more prevalent as a tool for retailers, for payments, loyalty and engaging with consumers in and out of the store, security of sensitive data becomes increasingly more important.

At first glance the message for banks from the latest World Retail Banking Report 2015 looks like very bad news for traditional banks. Globally, customers’ propensity to leave their primary bank is on the rise while their willingness to make referrals or buy additional products from their primary bank has decreased significantly.

Merchant Customer Exchange, developer of the CurrentC mobile payment platform has appointed financial services and payment industry veteran Brian Mooney as interim chief executive. Mooney succeeds Dekkers Davidson, who is leaving MCX to pursue other opportunities.

Security specialist RiskIQ says the growth in digital business is producing an increasing threat to banks across the world, with the largest banks owning an average of 7,500 public facing digital assets – 60% of which are outside the company firewall.

Host card emulation specialist Bell ID is enabling the launch of ANZ New Zealand’s upgraded goMoney mobile app, which is set to feature a cloud-based HCE NFC mobile wallet. The project, for the New Zealand division of ANZ Bank, will bring contactless mobile payments to the smartphones of more than 120,000 ANZ customers. The ANZ […]

Santander has launched the UK’s first standalone ISA mobile app , which was designed and developed with mobile specialist company Monitise.

Türk Ekonomi Bankası is to launch a mobile contactless payment application using Visa Europe’s host card emulation functionality to provide secure contactless payments.

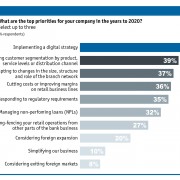

The need for a digital strategy has leapt to the top of retail banks’ agendas over the past year, replacing regulatory issues, as they look to fend of competition from tech and e-commerce rivals.

Ever since the deployment of Apple’s NFC solution – ‘Apple Pay’, and the various competitors launches since, there’s been speculation around what the future holds for consumer payments and how security will impact it

The Citi Mobile Challenge, which seeks to unearth innovation and developer talent in some of the most far flung reaches of globe in a bid to get the best talent to help change the way the world banks, has extended its registration deadline to allow more people to take part.

Mobile money is expanding rapidly as global smartphone penetration grows. This year, many providers are looking to expand their range of mobile money services to areas such as credit and savings – but operators must be wary of the remaining challenges, including regulation and market sizes, according to a new report by the GSMA.

Samsung has announced a new mobile payment service called Samsung Pay, that it claims will break the obstacles to mobile wallet adoption by being compatible with older point-of-sale terminals through the use of Magnetic Secure Transmission, which allows terminals using traditional magnetic stripe technology to accept payments.

As many more tech companies begin offering bank-like services, mainstream banks are searching for ways they can fight back

The mobile revolution is taking the financial services industry by storm. In less than five years it is predicted that the number of mobile phone owners using their device for banking purposes will double to over 1.75 billion. Banks cannot ignore the implications of what this means to their future business models. A mobile-first approach will be essential in leading the way.

Consumers in both developed and developing countries have embraced their mobile devices to check balances, make payments and conduct other financial activities. As a result, mobile banking has become a must-have offering for financial institutions. However, many are still working out how to go beyond the basics to add value for customers, increase engagement and maximise the return on the mobile channel investment.

One of the trends of 2014 was its delivery of technology that we had been promised for years but had fallen short until now. Siri, Cortana and Google Now all make good on the sci-fi staple of the voice-activated computer. Virtual reality has been attempted many times, but it seems that the Oculus Rift may have finally cracked it. And biometric authentication, while often included in devices but rarely used, is now commonly used by owners of new iPhones to unlock their devices thanks to Touch ID.

Widespread use of fingerprint authentication for financial transactions on mobile devices could start taking off from early next year as Bank of America, Wells Fargo, Google, Samsung, Lenovo, Microsoft, Alipay and others adopt a new authentication standard through their joint project, the FIDO Alliance, which has just published its specifications and launched its first server.

While online retailers roll their Black Friday bargains over to Cyber Monday, research shows that an increasing amount of online sales are being made via smartphones and tablets, and this trend is continuing – but this does not mean smaller crowds, as consumers are also switching to ‘click & collect’ services.

Monitise plans to raise £49.2 million through extensions of its relationships with Santander, Telefónica and MasterCard. The money raised will be used to ‘support the development and accelerated roll-out of its global platform capabilities’.

The time is right for a new breed of digital-only banks to enter the market and steal away share from the established players, according to a new report by Monitise.

Banks will be judged on how well they provide mobile services and social media interaction in the coming years. Instead of being just another channel, these forms will be the first point of contact for customers, according to a new report by analyst firm Celent.

While a great deal of attention has been given to Lloyds Banking Group’s retail operations as its various elements are split up, less has been given to its activities in transaction banking, where it is “one year into a three-year journey” to transform itself and its customer offerings to create“the best global transaction bank in this region”.

Banks and other financial institutions are finally spending more on growing new products in areas such as mobile and data analytics rather than maintaining legacy systems, according to a new report by Capgemini.

Citi has launched a global mobile challenge that it says will help to inspire technology developers to reimagine mobile banking and payments. The bank plans to host a series of events in Miami, New York and Silicon Valley in November, after which finalists will get the chance to bring their product to market with help from Citi.

The digital era is changing your bank rapidly. Is your mobile testing & assurance practice ready? P Venkatesh, director of the product division, and Srivatsan TT, vice president of the solutions group, at Maveric Systems discuss the issues

Despite the significant challenges faced by the UK’s banking sector over the last decade, there has been a dramatic evolution in the customer experience following the introduction of online, telephone and mobile banking. While the branch remains an important channel, especially for older customers, mobile technology is rapidly redefining how customers interact with their banks.

Apple may have lined up the chief executives of Bank of America and JP Morgan Chase to laud the launch of Apple Pay, but reaction from the wider industry was more muted – disappointed, even.

With the penetration of mobile devices, such as smartphones and tablets constantly growing, attention is increasingly turning to mobile marketing, mobile commerce and mobile payments. It is still the case, however, that these trends are largely played out in specialised media, and do not influence the actual behaviour of consumers. This is especially true for mobile payments, with consumers very sceptical about this concept

A new app-based social network that uses gamification concepts to train traders and help them to hone their skills has been launched by a former Deutsche Bank trader.

FinTech developers, designers and entrepreneurs are being challenged to a 36-hour development tournament in the days leading up to this year’s of the Money20/20 event in Las Vegas in November.

The mobile wallet is having a transformative effect on people’s lives in developing countries, bringing safer, faster, easier financial services to the people who need it most

Mobile NFC services continued to expand in 2013 but the big question is, will this be amplified or disrupted by the introduction of host-based card emulation (HCE) into mainstream operating systems?

Milan-based payment processing specialist SIA says that a migration of its systems to the Red Hat Linux environment has led to a 270% reduction in processing times.

David Sear, the former chief executive of the Weve mobile network e-commerce joint venture, has been appointed as group chief commercial officer at Skrill Group.

Analyst firm Juniper Research reckons more people will be using mobile apps for banking than web-based options by 2019, as the 800 million people who used their phones for banking more than doubles to 1.75 billion in five years.

Banks are continuing to spend money on branches, but they are dramatically changing their role to become centres for sale-oriented advice rather than service-oriented transactions, driven by the rapid growth of digital banking.

The annual transaction value of online, mobile and contactless payments will nearly double over the next four years, reaching $4.7 trillion by 2019, up from just over $2.5 trillion this year, with contactless payments primarily driven by card purchases rather than mobile.