Could banks become our 24/7 personal assistants?

Digital technology is on the verge of transforming banking, in a similar way that Spotify has completely changed the music industry and Netflix has revolutionised broadcast entertainment

Digital technology is on the verge of transforming banking, in a similar way that Spotify has completely changed the music industry and Netflix has revolutionised broadcast entertainment

Employment prospects in the UK finance and banking sector in the New Year are the brightest in the past three years as high profile data breaches, such as those at TalkTalk and Sony, create a surge in demand for cyber-security experts.

If the global payments industry were to be designed from scratch, nobody would design the system which we have today. Yet distributed ledger technology has the potential to bring about dramatic change– if it can overcome the unanswered questions over to what extent the industry should collaborate or compete and whether there will be one model or many different ones, according to speakers and delegates at the European Payments Regulation conference in London on Wednesday.

Quick business successes can be built on the UK’s payment system that will play a key role in encouraging the efforts required to ensure that it achieves the “world class” status the industry is aiming for.

One in five UK consumers (21%) have had personal details stolen and their bank accounts used to buy goods and services as a result of a cyber security breach, according to new research from business advisory firm Deloitte.

Trust – or more often, the lack of it – has become a recurring theme in financial services over the last few years. But if financial institutions really wanted to rebuild trust, they might start by looking at some of the safety improvements made by other industries such as the aviation industry, many of which rely on data, according to speakers at the Mondo Visione exchange forum in London.

UK regulator the Financial Conduct Authority is planning to launch a ‘regulatory sandbox’ that will allow businesses to test out new products and services without ‘incurring the normal regulatory consequences’. The move is part of the FCA’s year-old Project Innovate, which aims to boost competition and growth in financial services.

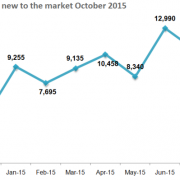

The news of major lay-offs to come put a dampener on otherwise good news in the financial sector jobs market in the UK last month. According to the Morgan McKinley London Employment Monitor, October saw an across the board increase in both new job opportunities and new job seekers.

Santander has launched a competition to support startups using distributed ledger technology in financial services. Through its subsidiary InnoVentures, the bank hopes to promote distributed ledger tools that could improve banking processes.

Banks should not kid themselves that they can simply appoint a ‘chief innovation officer’ and that will be enough to combat the threat posed by new technologies and the non-bank companies that are using them to steal business, warned panellists at the BBA conference in London on Thursday.

UK finance and accounting professionals have unrealistically high levels of confidence in their defences against security breaches – increasing the likelihood of such breaches happening.

One in three retail banking customers feel their mobile banking app is not as good as online banking through a browser, according to a new study by ecommerce company First Data in the UK. The figures also revealed that more than half still have yet to use a mobile banking app – suggesting that there may be both an unmet demand for more functionality in mobile apps, and a need to convince the remaining consumers of their value.

The London Stock Exchange Group is planning to launch a new interest rate derivatives venture called CurveGlobal, which initially aims to offer short term interest rate futures. Backed by several banks including Bank of America Merrill Lynch, Barclays, Citi, Goldman Sachs, JP Morgan and Société Générale, the new venture is part of the exchange’s long-held ambition to gain traction in the derivatives markets, which have historically been dominated by rivals in continental Europe.

Mobile transactions continue to increase their share of the market, accounting for up to half of online transactions, according to a new report by global payments technology company Adyen.

Three challenger banks have committed to take advantage of a new way to guarantee settlement between banks of payments made through Faster Payments, the UK’s 24/7 real-time payments service, when it becomes available next year.

Closer links between the Shanghai Stock Exchange and UK and European exchanges may be on the cards. The London and Shanghai exchanges are exploring a scheme to link their markets. At the same time, European exchange group Euronext announced a deal with the Shanghai Stock Exchange to promote its listed members to Chinese investors.

Online-only bank Fidor has launched in the UK, promising to change the way retail banking works by letting the customer build the services and products they want to use. The bank is part of a new wave of fresh banks entering the market, many of which focus their efforts online rather than on the high street.

UK building society Nationwide has begun a £500 million project to improve its branch network using NCR latest generation of self-service ATMs. The project aims to bring the kind of self-service experience customers can get at supermarkets to the retail bank branch.

The UK payment services market has been under the spotlight in recent months with the introduction of a new Payment Systems Regulator created with the intention, amongst other things, of opening up the industry to new and emerging payment service providers.

The Payment Systems Regulator, the new economic regulator for UK payment systems, today confirms the line-up of the Payments Strategy Forum it has set up to set the strategy for innovation in payment systems where the industry needs to work together.

Barclays has launched a cloud-based contingency payment service for corporates, which the bank says will help corporates to make payments even if they are unable to use their primary channel, for example during an internet outage. The deal comes as financial institutions and corporates increase their focus on risk mitigation.

Figures from Link, the UK’s cash machine network, show that the number of ATMs in the UK reached 70,180 in July, passing 70,000 for the first time. ATM figures from July, show that the total amount withdrawn from cash machines in July 2015 was £11.3 billion, up 4% compared with July 2014.

More than £2.5 billion was spent in the UK using contactless cards in the first half of 2015 and this is likely to increase even more as the upper limit for contactless payments increases from £20 to £30 from today.

The UK payments industry and regulators should focus on four main priorities to ensure the country has a ‘world class’ payments framework, according to Payments UK.

Equifax, the consumer and business information specialist, has launched a new service providing real-time, integrated data on companies and the individuals who own and run them.

No one involved in the UK financial services industry could have failed to notice the recent increase in level of fines issued by the UK’s City Regulator, the Financial Conduct Authority. Mary Stevens, from risk and regulatory technology company Wolters Kluwer Financial Services, analyses what the fines mean for the industry.

UK digital-only bank Atom has chosen financial technology company IRESS to provide the basis for its mortgage platform. Atom received its licence in June and plans to launch later this year.

Reports of the death of cash have dominated the 2015 news agenda. A variety of industry developments – from the launch of Apple Pay through to a Danish proposal to end the obligation of retailers to accept cash – work together to imply that paper notes and coins could soon lose relevance. All this is underpinned by apparently irrefutable stats from the Payments Council which reveal that cashless transactions have now overtaken the use of cash in the UK

Fintech association Innovate Finance has launched UK Fintech 2020, a manifesto that sets out goals for the UK to be a centre for financial services. These include calls for increased investment in fintech, efforts to attract more fintech firms and the creation of more jobs in the sector.

A new venture plans to create a multi-asset, multi-currency institutional payment and settlements infrastructure based on blockchain technology. Called SETL, the venture is backed by Peter Randall, former chief executive at Chi-X, the multilateral trading facility that is now part of BATS, and Anthony Culligan, founder of peer-to-peer bitcoin trading site Roolo.

The Plato Partnership, a consortium of asset managers and broker-dealers working to build a non-profit equities trading utility in Europe, has chosen the London Stock Exchange’s Turquoise subsidiary as its preferred partner, and the two companies announced they are exploring a “commercial collaboration”.

More than a million people switched their current account to a rival bank in the year leading up to July 2015, according to new figures published by UK payments system Bacs. The numbers represent only a minimal increase on the year before – undermining hopes that making switching easier would lead to dramatic improvements in the competitiveness of UK retail banks.

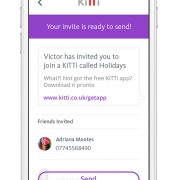

Santander has launched a group money management app called KiTTI, which is a virtual ‘cash kitty’ that allows groups of people to create a collective pot of money using a mobile app and a prepaid contactless MasterCard.

Ten financial services startups have been chosen by startup accelerator Startupbootcamp FinTech to participate in its annual London program, which seeks to find the best new companies in financial services and bring them to market. Notable themes among the finalists include Bitcoin and the blockchain, big data, algorithms, cloud computing and social networking.

Nearly half of UK consumers say that faster payments are a factor in their choice of back account provider, with 45% saying that the offer of faster electronic payments would encourage them to switch their bank account provider.

Recent studies suggest that banks in the UK are rebuilding their reputation among consumers and investments in mobile and digital are at least in part responsible –though trust remains fragile and other studies highlight concerns over pricing and transparency. Customer satisfaction across all sectors in the UK has flat-lined over the past six months, but some that regularly attract scrutiny – including banking – have shown signs of improvement,

BNP Paribas has become a direct participant in CHAPS, the UK’s same day high-value electronic payment system, the 22nd bank to join in this role. More are expected to join by the end of 2016. As a direct participant, the bank can directly send and receive irrevocable, guaranteed sterling payments with same day finality, rather than through a third-party.

UK banks rank bottom in a nine-country survey of how well banks match up to customer expectations in terms of rewarding customer loyalty and helping them manage their finance. Overall, the UK banks rank third, behind the US and Germany.

The Payment Systems Regulator, the new economic regulator for UK payment systems, has appointed Ruth Evans as the chair of the Payments Strategy Forum. Evans is currently chair of The Authority for Television on Demand, the independent co-regulator for the editorial content of UK video on demand services.

Apple Pay has launched in the UK without the participation of HSBC and Barclays, two of the UK’s largest retail banks.