Fintech Trends: the Expected, Unexpected and What’s Next at FinovateFall

Get a sneak peek at what trends will shape the discussion at FinovateFall, including a few things you might not expect.

Get a sneak peek at what trends will shape the discussion at FinovateFall, including a few things you might not expect.

Summer’s almost over, but there’s still time to play in the sand. Our decision to open our sandbox for all developers, not just clients, is a vital move in supporting creativity and innovation in payments. And, it’s speeding time to market.

Meet our No. 1 on the Top 5 Best Challenger Banks list and find out why CEO Rich Wagner says the company belongs there.

In the most recent InsurTech Bytes podcast, Sarah Greasley, CTO, Direct Line Group, opened up about her experience as a woman in fintech, the challenges and the solutions. FinTech Futures (Banking Technology’s sister company) uncovered the solutions for five of the key hurdles in her career. 1: Entrepreneurship and empowering risk taking Challenge: From a […]

Scott McInnes, partner at international law firm Bird & Bird, discusses how the Second Payments Services Directive (PSD2) will affect companies and what requirements industry players need to know.

It’s hard to imagine a fintech or payments company that today doesn’t have at least one key business initiative hinging on some kind of software development. Before you sign on the dotted line with a developer, here’s what you need to consider.

Nations, platforms and some bad news in our latest blockchain and bitcoin roundup. Find out more about the SEC’S suspension of First Bitcoin Capital Corp., an initial coin offering for cryptocurrency exchange platform KyberNetwork and more.

“There’s a reason that the bank of the future hasn’t been created yet—it’s extremely difficult,” says Top 5 Best Challenger Bank Varo Money. See if you think they’ve got what it takes to rise to the challenge.

Prepaid cards and alias-based payments that rely on email or mobile phone numbers can offer students and colleges and universities significant benefits over traditional check disbursement of financial aid.

The US Department of State recently released a report that identified mobile money services as particularly susceptible to money laundering in Africa. It cites services like M-PESA and M-Shwari as “services [that] remain vulnerable to money laundering activities”.

Designing the user experience consumers expect in digital banking is less about seeing what sticks and more about seeing what stands up to real-world human examination and use.

A new study from Juniper Research is forecasting that more than half (53 percent) of global transactions at the point of sale will be contactless within five years, compared with just 15 percent this year.

Elizabeth Denham, the UK’s information commissioner, made an astute point when she recently called for senior bank executives to get the same cybersecurity training as front-line staff, following the global WannaCry ransomware attack. But implementing the kind of comprehensive cyber defence strategy which includes such training will require a monumental culture shift at the top.

Plagued by delays, threatened by Congressional repeal and finally opened to further comment and changes, the CFPB’s final rule on prepaid accounts now has consumer groups calling for the bureau to “strengthen” consumer protections while a credit union trade group wants the rule rescinded.

It’s a rare ray of sunshine for the embattled Uber, as it won a key fight in the U.S. Second Court of Appeals, which ruled its terms and conditions (Ts & Cs) are legally binding

Six months after coming on board to lead the digital financial services trade association, Maikki Frisk talks about how to drive mobile payments adoption, the implications of Brexit and PSD2, and the ultimate importance of a good user experience.

Is fintech to banking what craft ale is to brewing? If so, what can banks learn from the rise and rise of craft ale? Aden Davies, principal consultant at ABZD, looks at ten trends seen in the craft ale industry that have interesting parallels with the rise of fintech.

It’s safe to say mobile is just getting started as a payments form factor, but don’t chuck your plastic cards just yet. Personalization, including QR codes, can boost usage and help you stay top of wallet.

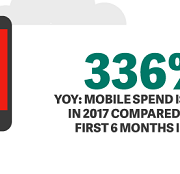

Mobile contactless transactions in the U.K. topped £370 million (US$476 million) in the first six months of 2017, a whopping 336 percent year-on-year increase, according to the latest transaction data from payments processor Worldpay. (Infographic included.)

With standards as simple as what we see with shipping containers, creative folks will begin considering options for almost anything that can benefit from these containers being mobile. The user experience that today we enjoy with mobile devices has changed the very heart of today’s data centre even as we see on-premise IT moving to clouds. Couldn’t a case be made that such flexibility be embraced even more aggressively in the future and couldn’t that change the very way we view banking as it continues to transform?

In the P2P showdown, who will be left standing? See how early entrants like Venmo and Square Cash stack up against Zelle and Apple.

As expected, U.S. Sen. Elizabeth Warren (D-Mass) is not going to let the CFPB’s final rule on arbitration agreements go down without a fight. The ranking member of the Senate Banking Committee’s Subcommittee on Financial Institutions and Consumer Protections wants big banks—not just their lobbyists—to address the issue.

In the age of the internet, fintech dominates finance. In the UK, the sector is currently worth £7 billion, employing around 60,000 people with figures set to increase. The industry is definitely awe-inspiring, but as the lines between traditional banking services and fintech blur, fintech could disappear entirely.

Former financial ombudsman Walter Merricks is appealing the U.K.’s Competition Appeal Tribunal’s decision not to certify his claim in a proposed £14 billion (US$18.2 billion) class action lawsuit against Mastercard over interchange.

Amid the hustle and bustle of MoneyConf in Madrid, Banking Technology managed to grab a coffee with Matteo Cassina, global head of sales at Saxo Bank. Conversation turned from the demise of bank branches to the rise artificial intelligence (AI) and open banking.

Take a lesson (and an infographic) from the Ohio University School of Economics on how to approach millennials and turn them into lifelong customers.

The EU Funds Transfer Regulation 2015 (FTR 2015), which has been in effect since 26 June 2017, aims to deliver full traceability of payments. A lack of regulatory clarity is, however, leading to significant implementation hurdles that require urgent action from all stakeholders.

Prepaid is having a renaissance thanks to real-time mobile and web account access that’s enabling a number of disruptors to offer prepaid solutions for a new set of customers.

Off the back of its involvement in Australia’s New Payments Platform (NPP), Swift has entered the instant payments market in Europe, with plans to launch a gateway solution in November 2018. The solution will enable instant payments to be made over the Swift network using a single gateway to connect to multiple instant payments systems across Europe.

The CFPB has released a new overdraft study, along with four prototypes of “Know Before You Owe” disclosures, which the bureau is testing, possibly ahead of regulating checking account overdrafts.

“We’ve got a great idea we think you’re going to love.” Despite its manifest flaws, this is the approach that has long dominated the development of new products and services. While introducing products that people love is an exemplary goal, real omniscience has proven to be distressingly rare.

Banks are investing in immediate payments to drive revenue, while focusing their IT investments on fraud prevention and operational efficiency, according to new benchmark data from ACI Worldwide and London-based consultancy Ovum.

Prepaid issuers should look to certain banked consumers, P2P and mobile wallet users to gain top-of-wallet status with a whole new set of customers.

It’s no secret that increased regulations are a significant pain point for commercial and community banks. According to Thomson Reuters Global Cost of Compliance 2016 Survey, more than one-third of participating financial institutions reported spending at least an entire day each week keeping track of regulatory changes. The good news? Regtech, or regulatory technology, is […]

The CFPB issued a bulletin July 31 warning companies about tricking consumers into expensive pay-by-phone fees. The bureau says it’s concerned about companies potentially misleading consumers about the purpose and amount of certain pay-by-phone fees or “keeping them in the dark” about much cheaper payment options.

In the beating business heart of London, Banking Technology met Ben Brabyn, head of tech hub Level39, for an exclusive interview on Brexit, rivalry and how success isn’t a zero-sum game.

Recent research from Blackhawk Network reveals that mobile and contactless payment options can help brands to engage with consumers by driving traffic and incremental sales, reducing shopping cart abandonment and supporting customer acquisition.

From Bitcoins to even newer (and lesser known, but rising) forms of currency, will this level the playing field for people in the future, or is this all just a sham that will die down? As things get digitised, what do we need to know about digital currencies, and does this mark the demise of traditional forms of currencies?

For any organization regularly processing card-not-present (CNP) payments, boarding the fintech bandwagon is a must. There are three key fintech developments—APIs, regtech and cybersecurity strategies—you need to embrace (or face disruption).

The U.S. House of Representatives voted on July 25 in favor of HJR 111 to repeal the CFPB’s final rule on arbitration agreements. The vote was 231-190, but the companion resolution in the Senate may be on the back burner for a while as the Senate focuses on budget and health care battles.