How the bank of tomorrow engages its customers today

Customer proposition depends on a data driven approach designed for early adopting, millennial professionals.

Customer proposition depends on a data driven approach designed for early adopting, millennial professionals.

Predicting what will happen to Bitcoin and other cryptocurrencies has become a cottage industry.

The landscape for financial services is changing, and the jury is still out on how the endgame is going to play out.

The digital currency is making a surprising entrance into the mainstream financial world.

The next wave of technological transformation will be driven by the rise of wearable technology.

As regulations evolve globally, data has become both an essential currency and a pain point for financial institutions.

Fintech companies will find that they are a different kind of business in 2018 than they were in 2017.

The recent World Economic Forum (WED) report “Sweden could stop using cash by 2023”, says that the country is moving towards favouring cards and mobile payment apps. Yet retailers are expected to accept cash for at least a couple of years afterwards.

To reap the real benefits of technology, treasurers should be thinking about an extended journey, not a day trip.

We are living through a period of unprecedented innovation in finance, and regulators know they need to adapt to keep up with the fast pace of change. To understand and manage the risks posed by new products, services, and business models, many financial authorities are setting up regulatory sandboxes or reglabs.

One of the more entertaining aspects of this year’s Sibos in Toronto was the continuation of the rivalry between the event’s host, Swift, and distributed ledger technology (DLT) firm Ripple.

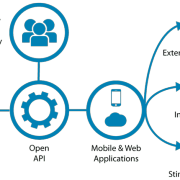

By adopting a layered model that moves the focus from presentation to orchestration, banks can deliver an omni-access digital service that truly works for customers, says Peter-Jan Van de Venn, CCO of Dutch digital core banking platform provider Five Degrees.

The uncertainty produced by the Brexit vote – and the turbulent negotiations since – has led some to question whether the UK can maintain its status as a global fintech capital. But for London as much as for its rivals in the US, China and beyond, the key may lie in capitalising on the next competitive edge for fintech centres.

There is a misconception about blockchain in the industry surrounding the belief that it is a solution to making faster and securer payments. There are some issues around the blockchain that explain why, in its present form, it isn’t an ideal replacement.

Swift’s global payments innovation (gpi) has taken giant steps towards solving many of the challenges corporates have faced with cross-border payments.

Amid the hype around distributed ledger technology and blockchain it can seem they are technologies looking for solutions. In the heavily paper-based business of trade finance, such technology looks promising and progress is being made elsewhere.

The global correspondent banking network is under pressure in several countries as some financial institutions close relationships. While financial inclusion continues to climb the agenda of regulatory authorities and financial institutions pledge their support, the de-risking taking place in correspondent banking threatens to scupper inclusion.

Ensuring security on Swift’s network doesn’t have to be rocket science. Getting the basics right will help individual institutions and Swift’s community.

With new banking reform on the horizon, Amit Dua, president of Suntec Business Solutions, assesses why customers will improve their financial and life circumstances if heritage banks and young fintech firms find a way to combine their strengths.

As financial authorities express concern about de-risking in correspondent banking, a similar phenomenon is emerging in trade finance, driven by the high costs of KYC compliance.

Financial technology has the potential to radically transform the securities industry. The fast pace of change could lead to disintermediation, according to an Iosco study.

Regulatory technology (regtech) is often cited as the answer to the rising cost of compliance, risk and reporting duties at banks. Will it help financial institutions escape IT silos and enhance control over data?

With myriad domestic instant and real-time payments systems being deployed internationally, is the next logical step cross-border, real-time payments? We asked some Sibos delegates what they think.

Discussing the strategies banks can adopt to choose the right innovation partners.

Escalating customer expectations, regulatory requirements and technological developments are fuelling the need for instant payments. Market providers agree that real-time payments will be the “new normal” and, it’s not a matter of if, it’s a matter of when.

As part of its global payments innovation initiative, Swift and a group of banks have been trialling distributed ledger technology (DLT) in the reconciliation of nostro databases in real-time.

Many financial services industry firms are examining the potential of distributed ledger and artificial intelligence (AI) technologies. Is it too early for any meaningful deployment?

Cybersecurity has become a significant issue as attacks are increasing. In the new payments ecosystem, where third-party developers can directly interact with banks’ customers, data privacy and security become paramount, according to the World Payments Report 2017.

Innovative technologies are increasingly sparking enhancements to trade processes. BNY Mellon Treasury Services’ Dominic Broom, global head of trade business development, and Joon Kim, head of global trade product, discuss how the industry – with banks at the helm – can drive forward new capabilities and help to support trade growth through digitalisation.

Much of the focus for correspondent bankers at this year’s Sibos will again be Swift’s global payments innovation (gpi) initiative. More than 110 transactions banks from Europe, Asia Pacific, Africa and the Americas have signed up to the initiative, which opened for live payments in January 2017.

Marketplace banking has the potential to deliver an interconnected financial services industry where banks can get closer to their small business customers explains Five Degrees’ Peter-Jan Van de Venn.

Marisa Kurk, senior managing director and COO of Mesirow Financial Currency Management group, explores best practices in foreign exchange (FX) settlement.

Rather than being top of wallet, SPENT Money wants to help consumers manage and earn rewards from what’s already there—at least for now.

Why would a bank let their corporates indulge in setting up system privileges online – without keeping close tabs on the process? Here’s why.

Acting Comptroller of the Currency Keith Noreika told FinovateFall attendees in New York this week that the agency is still in the exploratory phase of its fintech charter, according to news reports.

Payment Systems Regulator (PSR) and Bank of England have revealed that the U.K. will be getting the New Payment Systems Operator by the end of 2017, which the PSR says will be an important step in streamlining the U.K.’s payment systems and fostering competition and innovation.

The introduction of new bond requirements for money transmitters in Pennsylvania is in line with an overall trend across states to enforce stricter conditions on money transmitter license holders and applicants. See what the licensing requirements mean for your business.

At the recent G20 meeting in Germany, Financial Stability Board (FSB) briefed leaders on its efforts to arrest the decline in correspondent banking relationships. FSB also presented the results of a survey of more than 300 banks in 50 countries, supplemented by Swift payments data, which showed that the number of correspondent banking relationships continues to decline globally.

The landscape of cross-currency (FX) payments is taking on a whole new look – creating challenges for corporate financial managers and the need for new banking solutions.

It’s been seen as the ultimate clash of cultures. The baseball cap and T-shirt versus the formal suit and tie; the young, quick-thinking fintech versus the risk-averse multinational corporate; David versus Goliath.