Authorities Smash Hacking ‘Hornet’s Nest’ (July 16, 2015)

A major online hacking forum and malware marketplace has been shut down in a coordinated operation by law enforcement officials in 20 countries.

A major online hacking forum and malware marketplace has been shut down in a coordinated operation by law enforcement officials in 20 countries.

The release in 2013 of Universal Rules for Bank Payment Obligation by the International Chamber of Commerce effectively endorsed and formalised the structure for international trade finance processes. Despite this, the volume of completed BPO transactions remains low

It’s now law, but not all of the act is in force yet.

Regulated entities that verify identity in connection with the issuance of stored value cards may find more flexibility in the principle-based approach to identity verification outlined in the proposed regulations.

As retailers prepare for the year’s biggest gifting season, there are some key principles to guide digital gifting strategies that maximize revenue and loyalty.

advances in technology, and particularly consumer demand, are driving change and making the payments environment an interesting place to be in the years ahead

Public sector programs usually offer predictable loads and transaction volumes, and that information can be a plus. But reliable load patterns don’t guarantee overall success, especially if you price yourself out of profitability and sustainability.

Unless you’re a mathematician or a bitcoin fan, trying to understand what Ripple is—and why it’s so revolutionary—requires a bit of research (not to mention a double espresso!). That being said, here at Hyperwallet, we definitely think this new technology is worth investigating. In fact, I’d wager a bet that, within just a few years, Ripple could become as important to the world of payments as the Internet is to the world of information today.

The NBPCA’s newly elected president and CEO spoke with Paybefore about priorities, what happens behind the scenes of the association, and the work that lies ahead for an industry that must continue to raise awareness on the Hill.

Since the financial crash retail banks are faced with more regulatory and financial restrictions than could have been envisioned. This is coupled with increased levels of competition and much reduced consumer trust. Intelligent analytics may offer part of the solution.

Over the last decade the financial markets industry has experienced significant regulatory upheaval. We have witnessed a new approach to supervising financial institutions, with regulators moving from a “light touch” approach to an “interventionist” one

Popmoney, Dwolla, Square Cash, Funding Circle, Venmo, Nutmeg, Transferwise, Stellar, Kabbage … this is not a list of the latest box office hits or some weird shopping list, but a handful of the emergent FinTech companies that are sprouting up everywhere like wild mushrooms. These companies are, to a certain extent, beginning to reshape and […]

It seems not a day goes by without seeing those three little letters and five numbers – ISO 20022 – appearing in headlines or articles. But hang on a minute, what’s all the commotion about? It’s just another message format that I need to make sure my systems can handle, right?

Chris Larsen, chief executive of Ripple Labs, talks about his concept of the Internet of Value, and why his company is not a disruptor …

Cloud-based technologies are spreading rapidly through the business world: the research firm IDC expects the cloud software market to be worth more than $100 billion by 2018, implying compound annual growth of more than 21%, roughly five times faster than traditional packaged software. It is clear that cloud computing is on course to become an […]

Cybercrime investigators from six European countries joined forces and recently busted a large gang of cybercriminals that had used malware in a widespread attack on online banking systems across the Eurozone, resulting in losses of at least €2 million (US$2.22 million), according to Europol, the EU’s law enforcement agency.

JPMorgan Chase is changing its policies to offer more customers access to mainstream payment services—and the company’s Liquid prepaid card will play a key role in the initiative.

The global financial crisis devastated the reputation of the UK banking industry and it is not hard to understand why public trust in banks is at a low ebb. Since 2008, there have been at least five major scandals involving one or more banks operating in the UK, writes Peter Duffy Along with the reputational damage […]

Talking used to be a positive thing. For many years, BT reminded us that it was “good to talk”; whilst in the 1980s the Midland Bank (since acquired by HSBC) promoted itself extensively as “the listening bank”. Now, there is a new breed of bank coming to the UK; one that doesn’t have branches or want a ‘physical’ interaction with its customers

Tactical regulatory firefighting has distracted banks from their long-term strategic shift to an enterprise view of data. Looming issues such as the possible Brexit highlight the urgency of this task

Identity verification by financial institutions is necessary—but it doesn’t have to be a necessary evil. Combining mobile technology with knowledge-based authentication can help improve activation rates with a process that’s simple for the cardholder and secure. Here’s how.

As the consumer demand for remote login and flexibility continues to rise, organizations are struggling to find and deploy authentication methods that are effective, easy to use, impervious to theft and scalable. Say hello to biometrics.

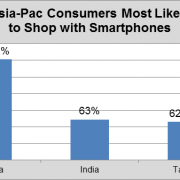

Mobile shopping is growing fast in the Asia-Pacific region, according to a newly released study by MasterCard.

The need for financial institutions to accurately gauge their exposure to myriad sources of risk has seldom, if ever, been greater. The credit crisis toward the end of the last decade must have made that clear, and if bankers managed to avoid getting the message back then, the point has been driven home ever since by regulators around the world

Seven and a half years ago, I wrote my first communication as the CEO of Paybefore, and now I’m writing my last. I’ve made the very difficult (but exciting) decision to retire from Paybefore.

For the new banks now is the chance to disrupt the banking industry. No legacy systems or existing processes or old thinking – they can jump straight to the new. Except, of course, those new banks that are being spun out of existing banks, where that infrastructure, IT and operations are supported by the current systems of the existing bank …

Regulators should not define how markets are structured when it comes to innovation and open access to clearing. Instead, it should be left up to the market to define how services are provided, according to speakers at the IDX FIA Europe conference in Europe this week.

A multi-agency federal regulator report concluded that the CFPB and prudential regulators are “generally” coordinating their oversight activities pertaining to consumer financial laws, consistent with the Dodd-Frank Act and the provisions of a MOU (memorandum of understanding) governing coordination activities.

Financial services has come under huge pressure in recent years particularly since the financial crisis. Competition, silo’d business units, efficiency in operation, compliance are just a few key issues being raised. With efficiency and competitiveness hand-in-hand and customer service as a bi-product of this, business process management (BPM), has shown just how this solution has driven cost efficiencies and overall resource efficiencies down.

The FDIC draws attention to a standard fraud claim without offering much guidance.

The increasing dependence of financial services on technology provides huge opportunity for IT vendors, but it also increases the supplier risk that these firms will carry, so it would be reasonable to expect the procurement process to become more rigorous.

What does this mean for vendors trying to sell into banks and other financial services businesses?

EU lawmakers reached a political consensus last week on a proposal for a new EU Payment Services Directive (PSD2). This follows several months of negotiations between European Parliament, the Commission and the Council of Ministers and marks a significant step in regulatory development within the payments market

For the first time since the financial crisis, banks are investing in digital strategies. That’s a step in the right direction, but how banks incorporate mobile into those strategies, ultimately, will determine their success.

Google’s open approach contrasts starkly with Apple’s, which has continued to maintain tight control over all integrated hardware and software components. But what does Android Pay really mean for banks?

With reports suggesting hackers have siphoned off up to $1 billion from 100 banks across 30 countries as part of a targeted attack, there are heightened concerns over the cyber-threat facing the banking sector. Supply chains are a potential weak link and banks have been stepping up their pressure on vendors and suppliers to do more to protect themselves from online intrusion.

Cybercriminals are using a new form of malware to steal shoppers’ personal financial data, according to an FBI alert issued to retailers last week.

The ability to browse limitless shops and purchase goods and services from almost anywhere in the world has revolutionised commerce. Yet this revolution is unfinished because no matter what the choice, no matter what the shopping experience, the critical moment of entering personal and payment details can be so complex and lead to the customer abandoning the sale

In the digital age, banks must adapt to new processes and customer expectations quickly. Yet many banks still operate legacy batch systems and have not yet transformed their ITO infrastructure. In association with SAP, Banking Technology is conducting a survey of the number of different systems banks have, and how long it takes for various transactions to occur.

Processors are poised to ignite innovation by rethinking traditional business models and devising solutions for an emerging customer-centered approach to payments.

When it comes to faster payments, the U.S. has reached a tipping point with new technology driving advances that are fueling consumer demand for real-time payments.