Canada Lays Framework for Digital Currency with New Regs (June 24, 2014)

While digital currency has received a frosty reception from many national governments, it has been greeted a bit more warmly in Canada.

While digital currency has received a frosty reception from many national governments, it has been greeted a bit more warmly in Canada.

Depending on who you speak to, the definition of a data scientist seems to mean different things to different people. Some see it as a glorified number crunching role, others believe the position requires someone more inquisitive to spot and respond to key trends.

CFPB Director Richard Cordray headed to the House yesterday to present his bureau’s semi-annual report to the House Financial Services Committee, headed by Jeb Hensarling (R-Texas).

The FDIC has issued another consent order for a company with significant prepaid business and again the focus is on Bank Secrecy Act (BSA) compliance.

In April, US post-trade utility the DTCC called for the US settlement cycle to be moved to T+2, to bring it into line with what’s happening in the rest of the world, which is converging on T+2 settlement cycles – at different speeds.

Despite promises of change heralded by the European Commission’s upcoming MiFID II, the cost of market data in Europe is still far too high and transparency remains a serious problem, according to senior financial industry executives. Yet the arrival of the Market Model Typology standard earlier this year may provide a catalyst for change.

A new generation of trading venues is competing their way into the European securities markets with plans to make trading more efficient. But will they bring benefit to banks and investors?

Could the establishment of an enhanced outsourcing oversight capability do more for asset managers than simply satisfy the FCA? A more mature set of oversight metrics could be used to provide foresight into how the outsourcer might perform in the future.

The Bancorp Bank, a wholly owned subsidiary of The Bancorp Inc., this week revealed in an 8K filing with the SEC that it’s stepping up its Bank Secrecy Act (BSA) compliance efforts in accordance with an FDIC consent order that went into effect June 5.

As the European Parliament adopted MiFID II/MiFIR on 15 April, the financial services industry was left wondering what exactly the new transparency regime is going to mean. Despite a curiously low EC estimate of compliance costs, at between €512 and €732 million, it is clear that MiFID II will have a large impact on the tens of thousands of firms and counterparties that will now fall under its scope.

Rather than spending time debating which option is worse for consumers—overdraft or payday loans—or focusing solely on reining in overdraft, we ought to shift our energies to creating new credit products that meet consumers’ needs transparently and affordably.

While asking a customer for multiple pieces of information and presenting him with various questions satisfies federal guidelines and other legal compliance, it can throw a major wrench in the prepaid card activation model. Out-of-wallet authentication must be accomplished in real time—and that means mobile.

The Consumer Financial Protection Bureau (CFPB) has bumped plans to release its proposed rule on prepaid cards to “the end of the summer,” according to Richard Cordray, the agency’s director.

Banking Technology first appeared 30 years ago this month. David Bannister, the current editor, looks back at that first year of coverage …

Shifting settlement cycles, the rise of big data, global regulation and increasing demand for post-trade services are creating both challenges and opportunities that global exchanges would do well to face wisely, according to Lars Ottersgard, head of market technology and Eva Saidac, head of business development market technology at Nasdaq OMX.

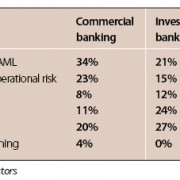

The past month has been a busy one for G-SIBs – global systemically important banks – as they confront the challenges of “what full compliance looks like” in the context of the Basel Committee on Banking Supervision and its Principles for Effective Risk Data Aggregation and Risk Reporting.

Reporting on the management of intraday liquidity risk will start on a monthly basis from 1 January 2015 to coincide with the implementation of the liquidity coverage ratio reporting requirements. Christian Goerlach of Deutsche Bank, takes a closer look at some of the issues facing global banks.

An question that continues to be asked is will the increased adoption of ISO 20022 facilitate the consolidation of payments clearing utilities and see the introduction of new services for customers? This suggests that despite the fact that ISO 20022 has been around for more than decade, confusion still exists over what it is.

The European Union and the larger international policy community have given substantial attention to anti-money laundering regimes this year, cueing both financial institutions and regulators to begin the race to implement and enforce respectively, writes Aamir Khan, general counsel and head of London office at Clutch Group.

More than six months into his new gig, CashStar’s CEO explains why the biggest potential for digital gift cards may lie in promotions, loyalty and customer service.

We have the opportunity to make a difference, to be part of the process and to influence the outcome of prepaid regulations.

Across the financial services sector, the question is now less about where cloud technology is being used, and more about where it isn’t used. Where do financial institutions draw the line when it comes to deciding whether to keep a process or IT-related service in-house or outsource it to specialists such as Amazon Web Services, SAP and many others?

The speed at which the mobile market evolves is staggering. Just as we started to look at mobile first, where banks need to align their services and strategies to cater for mobile before desktop or other traditional channels, the notion of mobile-only is now creeping to the fore.

The benefits of changing a payments portfolio over to a service provider with a modern and flexible platform are inherent and far outweigh the downside of staying with a provider whose solution is a poor fit.

Year one as the head of prepaid for Discover has led to some interesting lessons, including the importance of thinking beyond practical boundaries to create unique, workable solutions.

EMV chip card technology that helps block counterfeit card fraud at the POS is coming to the U.S., and last week I was one of the first on my block to experience it.

Given that bank customers are unlikely to increase significantly their usage of ATMs and now that opportunities to deploy large numbers of additional dispensers are limited, what does the future hold for the ATM and where does its next phase of growth lie?

If proposed changes to simplified due diligence go through as drafted, it will drive out a whole section of the prepaid market from Europe.

In a post-2008 crisis landscape dominated by regulatory reform, compliance is only part of the issue. If firms can address how they manage multiple data sets and deploy a truly enterprise-wide model, they can capitalise on the real opportunity – achieving a competitive advantage.

For the banking sector, which by definition at least is as much economic activity as it is social utility, the relevance of gamification is no longer debatable. Yet recent research shows that just 9% of banks globally have made forays into gamification

The capital markets industry continues to be amongst the top data driven industries. Electronic trading generates millions of market messages during a given day. With diminishing returns in high-frequency trading, focus has shifted from high-speed trading to looking for patterns in large volumes of market data for financial information and use cases.

Looked at from a data perspective, many new regulations have overlapping requirements that come back to customer data. Banking Technology joined forces with Markit І Genpact KYC Services and regulatory specialist JWG to look at how firms are approaching the challenges this poses.

GPR and payroll providers may be eager to take advantage of what the CFPB estimates will be $17 million in annual saving across the financial services industry. The proposed rule, however, may not be a real option for prepaid providers.

The central bank has pulled back on a mandate requiring new POS and ATM terminals to include biometric authentication. However, it’s also enabling prepaid providers, for the first time, to offer cashout at biometric terminals.

The work corporates are doing to streamline cash management processes should not end with SEPA implementation, says. Indeed, the principles and ideas underpinning SEPA can inform progress even in the most challenging markets.

While the logjam over EMV debit routing may finally be breaking up, it remains unlikely that EMV will reach the mainstream ahead of the liability shifts the payment networks plan to implement in October 2015.

Suggesting that investments in digital currencies, such as Bitcoin, might carry with them a higher risk of fraud and a harder time recovering losses in the event of fraud or theft, the SEC yesterday issued an investor alert regarding the decentralized P2P currency.

Although this lawsuit involves lending practices, the industry would be wise to pay close attention because of its UDAAP implications, which are applicable to all entities the CFPB regulates.

Rules issued last December by Canada’s Department of Finance affecting open- and closed-loop prepaid cards went into effect May 1.

The introduction of a financial transaction tax could mean London losing a swathe of banking business to financial centres with a lighter regulatory regime, such as Hong Kong or Singapore not to mention the logistical and technical challenges for banks.