US and Europe set for real-time payments by end of 2017

The US and eurozone countries both look set to have live real-time payment infrastructures by the end of 2017, both using the ISO 20022 for real-time messaging standard.

The US and eurozone countries both look set to have live real-time payment infrastructures by the end of 2017, both using the ISO 20022 for real-time messaging standard.

Complying with the European Commission’s Payment Services Directive II is like climbing the massive sandstone bulk of Ayers Rock in Australia – you think you’ve reached the top, and then you realise you still have a long way to go, according to speakers at the recent European Payments Regulation conference in London.

As part of the ongoing Basel reforms, the Bank for International Settlements is busy rewriting the rules that govern how much capital banks must maintain in order to mitigate different types of risk. So far the Standardized Approach for Measuring Counterparty Credit Risk Exposures and the Fundamental Review of the Trading Book have garnered the most attention. However, these are just two components of a much larger package of changes to the Basel capital requirements, which banks need to think about holistically and start factoring into their technology programs now

The UK’s Payment Systems Regulator has published draft guidance on its plans for regulating new European payment card legislations that comes into force next week.

Just under two-thirds of the world’s top nations in capital markets have now adopted international best practices, according to a new report on financial market infrastructures, but more work is needed on trade repositories.

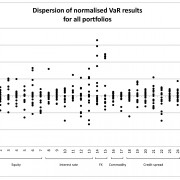

It’s no secret that past risk management practices and regulatory frameworks failed with respect to the global financial crisis. There were a number of reasons behind this, ranging from an overreliance on quantitative analysis to poor risk governance and frameworks, not to mention a lack of understanding around concentrated risk build-up such as leverage, convexity […]

Integrated stress testing is the preferred tool from a supervisory perspective. And that’s on a global basis. It may not be new, but it is featuring increasingly higher on the regulatory agenda and so understanding the technological opportunities is all important. A key building block for effective and integrated stress testing is an integrated balance sheet strategy

Financial market infrastructures must work with the “broader ecosystem” to improve the resilience of the international financial system in the face of “inevitable” cyber-attacks. The latest guidance document from the Committee on Payments and Market Infrastructures and the International Organization of Securities Commissions – Guidance on cyber resilience for financial market infrastructures – looks to […]

One in five UK consumers (21%) have had personal details stolen and their bank accounts used to buy goods and services as a result of a cyber security breach, according to new research from business advisory firm Deloitte.

De-risking, motivated by short-term risk-reward calculations, should not be allowed to kill off one of the cornerstones of the global financial system. Rather than abandon correspondent banking relationships, banks should be thinking about investing in and automating their risk controls, according to a new whitepaper by PwC.

Trust – or more often, the lack of it – has become a recurring theme in financial services over the last few years. But if financial institutions really wanted to rebuild trust, they might start by looking at some of the safety improvements made by other industries such as the aviation industry, many of which rely on data, according to speakers at the Mondo Visione exchange forum in London.

The European Commission has acknowledged that further delay to MiFID II may be ‘necessary’, following a letter from ESMA which said it would not be possible to implement the legislation in time. The delay follows an earlier setback in May and means the new rules could be delayed until January 2018.

UK regulator the Financial Conduct Authority is planning to launch a ‘regulatory sandbox’ that will allow businesses to test out new products and services without ‘incurring the normal regulatory consequences’. The move is part of the FCA’s year-old Project Innovate, which aims to boost competition and growth in financial services.

Recent years have seen unprecedented changes to the technical infrastructure of financial institutions. Many of these changes have been driven by regulatory mandates drawn up in response to the financial crisis of 2007/8. As the Global Systematically Important Banks battle to comply with the January 2016 deadline of the Basel III Directive BCBS239, it is […]

Global regulatory body the Financial Stability Board has released two guidance papers which aim to solve the “too big to fail” scenario and prevent a re-run of the financial crisis by promoting the resolvability of systemically important financial institutions.

Eight years on from the global financial crisis, and banks continue to face a growing number of challenges. Many have ceased or significantly reduced proprietary trading, with the resulting reduction in both risk and reward. This period has also seen lower risk appetite among many investors and continuing global competition which has put pressure on profit margins,

Banks should not kid themselves that they can simply appoint a ‘chief innovation officer’ and that will be enough to combat the threat posed by new technologies and the non-bank companies that are using them to steal business, warned panellists at the BBA conference in London on Thursday.

The fact that London’s financial services sector is also a hot spot for technology innovation is not news. In 2014, investment in financial technology firms grew by 136%. Earlier this year, George Osborne identified London’s financial technology sector as a particularly bright spot in the recovering economy – not surprising when you consider the transformational effect that information technology continues to have on the industry

Hasty unilateral moves by individual countries could undermine the ability of financial institutions and markets to benefit from new regulations and weaken efforts to improve financial stability, delegates at the BBA conference in London heard yesterday.

More transparency is urgently needed to restore trust in the FX industry, according to a new report by foreign exchange MTF LMAX Exchange – but to make that happen, the industry will have to collaborate.

Chrisol Correia, Head of Global Anti-Money Laundering Solutions, LexisNexis Risk Solutions

Compliance obligations are increasing for financial institutions. A utility approach to the issue is gaining favour …

It seems that at each Sibos, certainly since the financial crisis of 2008, a regulatory deadline is looming large. This year’s model is the Basel Committee on Banking Supervision’s (BCBS’) 11 principles for effective risk data aggregation and risk reporting (BCBS 239), with which globally systemically important banks (GSIBs) must comply by 1 January 2016. However, a report on the progress of adoption reveals a lack of preparedness.

Major financial market infrastructures (FMIs) and central banks have thrown their weight behind a Swift initiative to prevent further fragmentation of the ISO 20022 messaging standard as its adoption grows by signing a charter backing principles to harmonise implementations.

T2S, Europe’s harmonised settlement platform, is live. With a series of migration waves scheduled up until full live operation in July 2017, the next few years are likely to be characterised by intense activity as market participants finalise their strategies …

The Payments Market Practice Group has endorsed the use of Swift messages for intraday liquidity reporting. The Swift message set for intraday liquidity reporting underpins a rulebook created by the Liquidity Implementation Task Force, an industry group of twenty five large clearing banks, custodian banks and global brokers, to support compliance with Basel Committee on Banking Supervision requirements.

A large part of any financial technology businesses is clearly driven by the need for banks to comply with the ever-changing regulatory requirements that affect their business. And this has brought about a frenetic period of activity and growth in this core market. These changes affect the various individual areas within financial organizations Wolters Kluwer Financial Services and others serve, including Finance (e.g. IFRS9), Risk (e.g. Basel III Liquidity, FRTB) and Regulatory Reporting (e.g. CRD IV). They also impact the way in which these processes are governed and controlled centrally

South Africa’s Nedbank has chosen Volante Technologies to help it revamp its payments message service using VolPay Foundation, which focuses on validating and processing payments. The move comes ahead of regulatory change next year, which will force all South African institutions to change the way they handle payments.

JWG, the financial services regulation specialist, has appointed Blythe Barber as managing director as part of the continuation of the company’s expansion. Barber has been hired as part of an expansion of JWG’s RegDelta regulatory change management platform.

Sometimes the least obvious changes can have a big effect, and very often those changes are in areas that might considered outside the remit of the people best placed to make them. Bank staff remuneration, for instance …

Call it immediate, instant, fast(er) or real-time, the drive to speed up payments is being discussed in almost every country. As part of that discussion Banking Technology and ACI Worldwide brought together international participants from Australia, Europe, the UK and the US review the opportunities and challenges ahead.

The majority of businesses do not have cyber security insurance, with many not even aware such protection exists – and even those that do have insurance in place may find themselves at a loss if they don’t have the correct cover. The solution may be to mandate more data sharing and raise public awareness, according to speakers at a roundtable organised by software security company Kaspersky Lab.

A bank cannot hope to compete in today’s retail banking market without a ‘digital executive team’ and banks need to reinvent their upper echelons’ if this is currently lacking, as Atom Bank and Apple Pay are merely the start of an avalanche of a new era of digital disrupters, looking to steal the lunch from traditional high street banks.

Last year, the ISO 20022 standard celebrated its 10th birthday, and consequently it may seem a bit odd to say that after more than a decade since its inception, the financial community really should start taking assertive action. Since 2004, the ISO 20022 standard has, thankfully, witnessed substantial adoption but it has been what could be termed an “uncontrolled adoption”. So why is action so critical now?

Central banks need to play a greater role in the provision of infrastructure for low value payments and existing models revised to balance risk and rewards, according to new research published by the Swift Institute.

Russia’s central securities depository NSD has implemented back-to-back settlement technology for off-exchange delivery-versus-payment transactions with securities denominated in Russian rubles. The bank accounts and transactions may be in rubles, US dollar, Euro and Chinese yuan.

Barclays has launched a cloud-based contingency payment service for corporates, which the bank says will help corporates to make payments even if they are unable to use their primary channel, for example during an internet outage. The deal comes as financial institutions and corporates increase their focus on risk mitigation.

Data breaches are getting worse with 246 million records compromised by criminal activity in the first six months of 2015, according to new figures published by digital security company Gemalto. The numbers suggest cyber-crime will remain a top priority for banks for the foreseeable future.

The International Securities Services Association adopted a set of compliance principles to address the “critical challenges” posed by financial crime. The new principles aim to establish “a clear global standard for the opening and maintenance of cross-border securities accounts”.

As the SEPA deadline has come and gone, what will be built upon its advances towards digitisation and standardisation?